According to data from IRI, dollar sales growth for the total grocery store jumped up 63% in mid-March, compared to the same week in 2019. Individual departments also saw unprecedented growth, including the meat department, which had the largest jump with 91% dollar sales growth the week of March 22.1 Much of this business, as you know, was due in part to the closing of foodservice establishments across the country and consumers quarantining at home.

These unprecedented sales increases for grocery stores – and meat departments in particular – not only generated unexpected revenue, but also opportunities to service new customers.

“We were fortunate to have the opportunity to help our guests weather this pandemic and as a result, our business grew,” explained Mike Richter, vice president of fresh merchandising at Coborn’s, Inc., a Midwest supermarket chain. “At this point, we know we need to earn that business or we will lose it.”

Now, as we prepare for 2021, we cannot take our foot off the gas. It’s time to take what we learned this year, understand how the consumer has changed, tighten our messaging and up our branding. Each of these elements will be important to retaining the new business 2020 brought.

At Midan Marketing, we have been tracking shopping changes at the meat case since March with monthly consumer surveys. Some of the results, like the increase in stockpiling behaviors, are unsurprising given the overall narrative of the pandemic. But other results were less expected. For example, in September 33% of consumers reported eating more meat or chicken in the past month. The same number (about 1 in 3) say they plan to purchase meat primarily online once COVID-19 ends. And 3 in 5 shoppers think they will continue experimenting with new recipes and methods of cooking meat.2

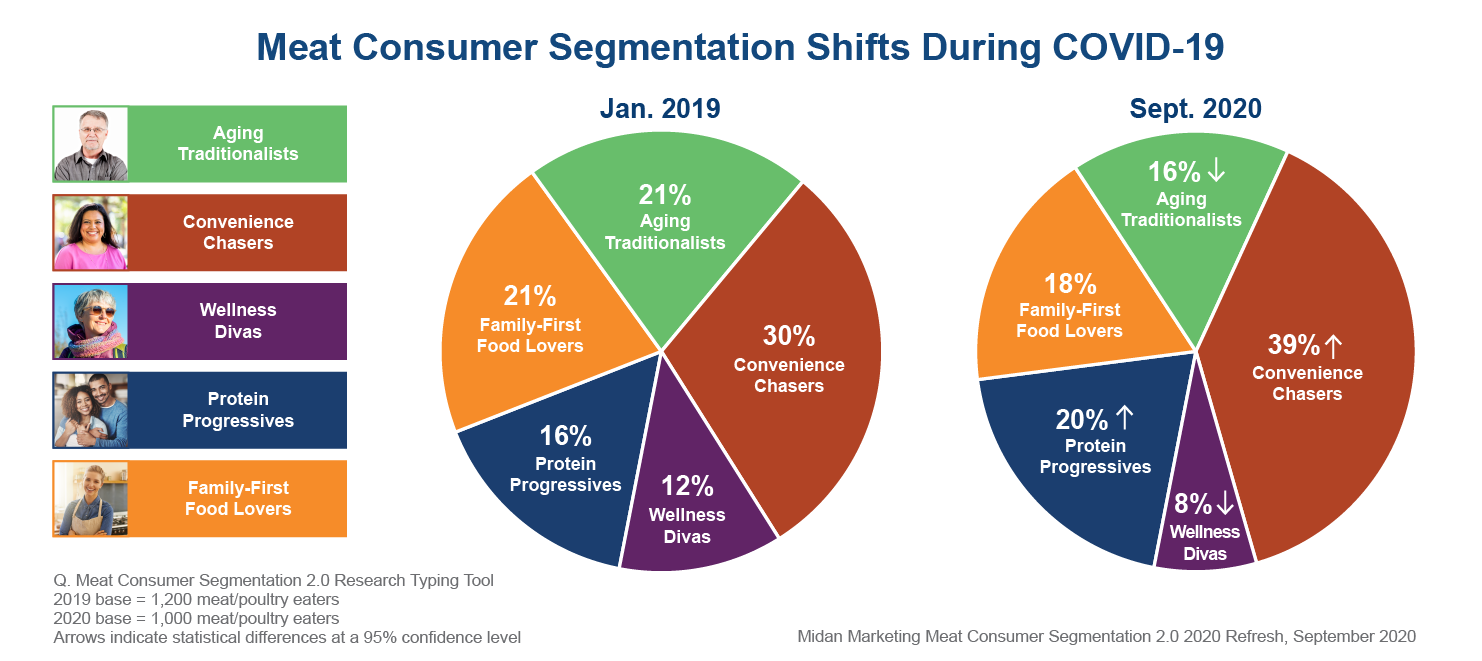

How do all these changes in behavior come together to give us an updated picture of the consumer? In 2019 Midan released our Meat Consumer Segmentation 2.0 research which highlighted attitudes and purchase behaviors of meat and poultry consumers. In September, we revisited that research to determine if the distribution of the meat and poultry consumer segments had shifted.

In 2019, the largest segment was Convenience Chasers, with 30% of meat consumers falling into this category. These are shoppers who are looking for convenience first and who are price-conscious, use coupons and seek out promotions. They are often time-pressed and looking for easy meal solutions. Given COVID-19’s effect on food prices and the rise in at-home responsibilities for many families, it’s no surprise that this is the segment that grew the most this year. Our September survey found that now 39% of the meat-consuming population falls into this category.5

The other segment that grew during the pandemic was the Protein Progressives. Previously comprising 16% of the population, this group of kitchen experimenters now accounts for 20% of consumers. These consumers likely tried their hand at sourdough bread in March and maybe even smoked their first backyard brisket over the summer. This segment loves all proteins, especially meat, but are adventurous in their eating habits, leading them to increasingly replace meat with plant-based proteins.

The Family-First Food Lovers segment stayed relatively the same over the last year, while the proportion of Aging Traditionalists and Wellness Divas slightly decreased.5

2 Midan Marketing COVID-19 Survey, September 2020

3 IBM 2020 U.S. Retail Index, August 2020

4 IRI, COVID-19 weekly survey of primary shoppers, Wave 12, 5/29-5/31/2020

5 Midan Marketing Meat Consumer Segmentation 2.0 2020 Refresh, September 2020

This content originally appeared in The Shelby Report.

Get additional COVID-19 Insights here